Take control of your future with effective strategies for managing student debt. Plan for repayment and minimize financial burden.

Take control of your future with effective strategies for managing student debt. Plan for repayment and minimize financial burden. Student debt can feel like a massive weight, a shadow hanging over your post-graduation dreams. But it doesn't have to be. With the right strategies and a proactive approach, you can manage your student loans effectively, minimize their burden, and set yourself up for a brighter financial future. This isn't about magic solutions; it's about smart planning, consistent effort, and understanding your options.

Understanding Your Student Debt Landscape

Know Your Loans Types and Terms

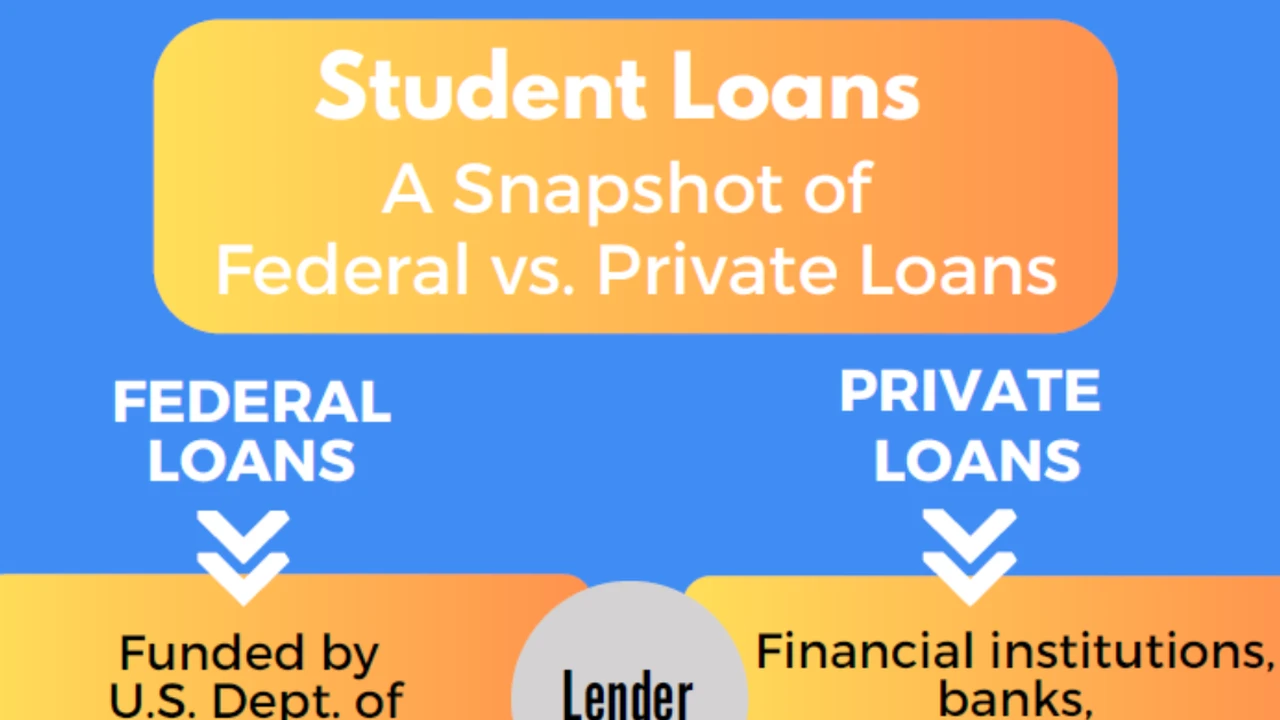

Before you can manage your debt, you need to understand exactly what you're dealing with. Student loans aren't a monolith; they come in different forms, each with its own rules and implications. The two main categories are federal and private loans.

Federal student loans are issued by the U.S. Department of Education. They often come with more flexible repayment options, interest rate benefits, and borrower protections. Examples include Stafford Loans (Direct Subsidized and Unsubsidized), PLUS Loans, and Perkins Loans (though Perkins is no longer disbursed).

Private student loans, on the other hand, are offered by banks, credit unions, and other financial institutions. They typically have fewer borrower protections, and their interest rates can be variable, meaning they can change over time. Understanding which type of loans you have is crucial because it dictates your available repayment strategies.

For instance, federal loans might offer income-driven repayment plans, while private loans generally do not. Knowing your interest rates, loan servicers, and repayment start dates for each individual loan is also paramount. You can usually find this information by logging into your loan servicer's website or the National Student Loan Data System (NSLDS) for federal loans.

Calculating Your Total Debt and Monthly Payments

Once you've identified your loan types, gather all the numbers. What's your total principal balance across all loans? What are the individual interest rates? What will your estimated monthly payments be once repayment begins? Many loan servicers provide calculators on their websites to help you estimate this. You can also create a simple spreadsheet to track each loan, its balance, interest rate, and estimated payment. This comprehensive view will help you visualize the full scope of your debt and plan accordingly.

Strategic Repayment Approaches for Student Loans

Income Driven Repayment Plans Federal Loan Benefits

If you have federal student loans and are struggling to afford your monthly payments, income-driven repayment (IDR) plans can be a lifesaver. These plans adjust your monthly payment based on your income and family size, often making payments more manageable. There are several IDR plans, including Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR). Each has slightly different terms regarding payment calculation, interest subsidies, and repayment periods (typically 20 or 25 years, after which any remaining balance may be forgiven, though it might be taxable).

To apply for an IDR plan, you'll need to submit an application to your loan servicer, providing documentation of your income. It's important to re-certify your income and family size annually to ensure your payments remain accurate.

Loan Consolidation and Refinancing Exploring Options

Federal Loan Consolidation Streamlining Payments

Federal loan consolidation allows you to combine multiple federal student loans into a single Direct Consolidation Loan. This can simplify your payments by giving you one loan and one loan servicer. It can also extend your repayment period, which might lower your monthly payment, though it could increase the total interest paid over the life of the loan. The interest rate for a consolidated loan is a weighted average of your original loans' interest rates, rounded up to the nearest one-eighth of a percent. Importantly, consolidation does not lower your interest rate.

Student Loan Refinancing Private Loan Strategies

Refinancing is different from consolidation. When you refinance, you take out a new loan, typically from a private lender, to pay off your existing student loans (federal, private, or a mix). The goal of refinancing is usually to get a lower interest rate, which can save you a significant amount of money over time, or to change your loan terms (e.g., a shorter or longer repayment period). However, refinancing federal loans into a private loan means you'll lose federal loan benefits like IDR plans, deferment, forbearance, and potential loan forgiveness programs. This is a big decision and should be carefully considered.

Several lenders offer student loan refinancing. Here are a few popular options and what they offer:

* Sallie Mae: A well-known name in student loans, Sallie Mae offers competitive rates for refinancing. They often have a variety of repayment terms, from 5 to 15 years. Their rates can be variable or fixed. Eligibility often requires a good credit score (typically 670+) and a stable income. They also offer a co-signer release option after a certain number of on-time payments.

* Typical Rates: Variable APR from 4.50% - 14.00%; Fixed APR from 5.00% - 15.00% (These are illustrative and can change based on market conditions and borrower creditworthiness).

* Best Use Case: Borrowers with excellent credit looking for flexible repayment terms and potentially lower rates.

* SoFi: One of the pioneers in online student loan refinancing, SoFi is known for its user-friendly platform and competitive rates. They cater to borrowers with strong credit profiles and offer both fixed and variable rates. SoFi also provides unemployment protection and career support services.

* Typical Rates: Variable APR from 4.75% - 13.50%; Fixed APR from 5.25% - 14.75%.

* Best Use Case: High-earning professionals with strong credit seeking competitive rates and additional borrower perks.

* Earnest: Earnest stands out for its flexible payment options, allowing borrowers to customize their payment schedule to fit their budget. They offer a 'precision pricing' model, which means your rate is highly personalized. They also have a unique bi-weekly payment option that can help you pay off your loan faster. Like others, good credit is essential.

* Typical Rates: Variable APR from 4.60% - 13.75%; Fixed APR from 5.10% - 14.50%.

* Best Use Case: Borrowers who value highly customizable payment plans and have strong credit.

* CommonBond: CommonBond offers refinancing for both undergraduate and graduate loans. They are known for their social impact initiatives (they fund education for children in need for every loan funded). They offer competitive rates and a variety of repayment terms. They also have a strong customer service reputation.

* Typical Rates: Variable APR from 4.80% - 13.90%; Fixed APR from 5.30% - 14.90%.

* Best Use Case: Borrowers looking for competitive rates from a socially conscious lender.

When comparing these lenders, consider not just the interest rate but also the repayment terms, any fees (though most reputable refinancers have none), customer service, and any unique borrower protections or benefits they offer. Always get quotes from multiple lenders to find the best deal for your specific situation.

Aggressive Repayment Strategies Paying Down Principal

If your financial situation allows, consider aggressive repayment strategies to pay down your principal faster. This can save you a significant amount in interest over the life of the loan.

The Debt Avalanche Method Prioritizing High Interest

The debt avalanche method involves paying off your loans with the highest interest rates first, while making minimum payments on all other loans. Once the highest-interest loan is paid off, you take the money you were paying on that loan and apply it to the next highest-interest loan. This method saves you the most money in interest over time.

The Debt Snowball Method Building Momentum

The debt snowball method focuses on paying off your smallest loan balance first, regardless of interest rate, while making minimum payments on all other loans. Once the smallest loan is paid off, you take the money you were paying on that loan and apply it to the next smallest loan. This method is less about saving money on interest and more about psychological wins, as you quickly eliminate individual debts, building momentum and motivation.

Deferment and Forbearance Temporary Relief Options

If you face temporary financial hardship, deferment and forbearance are options that allow you to temporarily postpone or reduce your student loan payments. However, it's crucial to understand the implications.

Deferment Understanding Interest Accrual

During deferment, interest may or may not accrue, depending on the type of loan. For example, interest typically does not accrue on subsidized federal loans during deferment. Common reasons for deferment include enrollment in school, unemployment, or economic hardship. You must apply for deferment and meet specific eligibility criteria.

Forbearance Interest Always Accrues

During forbearance, interest always accrues on all types of loans, including subsidized federal loans. This means your loan balance will grow even while you're not making payments. Forbearance is often granted for shorter periods and for various reasons, including financial difficulty, medical expenses, or other extenuating circumstances. It's generally seen as a last resort because of the accruing interest.

Both deferment and forbearance should be used cautiously and only when absolutely necessary, as they can increase the total cost of your loan over time.

Maximizing Your Financial Resources for Debt Management

Budgeting and Expense Tracking Finding Extra Funds

Effective budgeting is the cornerstone of good financial management, especially when dealing with debt. Create a detailed budget that tracks all your income and expenses. Use budgeting apps like Mint, YNAB (You Need A Budget), or Personal Capital to categorize your spending and identify areas where you can cut back. Even small savings can add up and be directed towards your student loans.

Side Hustles and Additional Income Boosting Repayment Power

Consider taking on a side hustle or finding ways to earn additional income. This extra money can be directly applied to your student loans, accelerating your repayment. Options include freelancing, gig economy jobs (like ride-sharing or food delivery), tutoring, or selling unused items. Every extra dollar you put towards your principal can reduce the total interest you pay.

While not applicable to everyone, several student loan forgiveness programs exist, primarily for federal loans. The most well-known is Public Service Loan Forgiveness (PSLF), which forgives the remaining balance on Direct Loans after 120 qualifying monthly payments are made under a qualifying repayment plan while working full-time for a qualifying employer (government or non-profit).

Other programs include Teacher Loan Forgiveness, which can forgive up to $17,500 for eligible teachers, and various state-specific or profession-specific programs. Research these options carefully to see if you qualify, as they can significantly reduce your debt burden.

Long Term Financial Planning Beyond Debt Repayment

Building an Emergency Fund Financial Security

Even while aggressively paying down debt, it's crucial to build an emergency fund. Aim for at least 3-6 months of living expenses saved in an easily accessible account. An emergency fund acts as a buffer against unexpected expenses (like car repairs or medical bills), preventing you from going further into debt or missing loan payments.

Investing for the Future Wealth Accumulation

Once you have a solid emergency fund and a manageable debt repayment plan, start thinking about investing. Even small, consistent investments can grow significantly over time due to compounding. Consider contributing to a retirement account like a 401(k) (especially if your employer offers a match, which is free money!) or an IRA. Diversify your investments and consider your risk tolerance.

Credit Score Management Maintaining Financial Health

Your credit score plays a vital role in your financial life, impacting everything from loan interest rates to apartment rentals. Make sure to pay all your bills on time, keep your credit utilization low, and regularly check your credit report for errors. Responsible student loan repayment can positively impact your credit score, opening doors to better financial opportunities in the future.

Managing student debt is a marathon, not a sprint. It requires patience, discipline, and a clear understanding of your financial landscape. By implementing these strategies, you can take control of your student loans, reduce their impact on your life, and build a strong foundation for your financial well-being.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)