Comparing Student Loan Options Federal vs Private

Understand your borrowing choices with our comparison of student loan options, federal vs private. Make informed financial decisions.

Understand your borrowing choices with our comparison of student loan options, federal vs private. Make informed financial decisions.

Comparing Student Loan Options Federal vs Private

Navigating the world of student loans can feel like deciphering a complex financial puzzle. For many students, especially those heading to college in the US or looking to study abroad in the US from Southeast Asia, understanding the differences between federal and private student loans is absolutely crucial. It's not just about getting money for tuition; it's about making smart financial decisions that will impact your life for years to come. Let's break down these two main types of student loans, compare their features, and help you figure out which might be the best fit for your academic journey.

Understanding Federal Student Loans Your Government-Backed Options

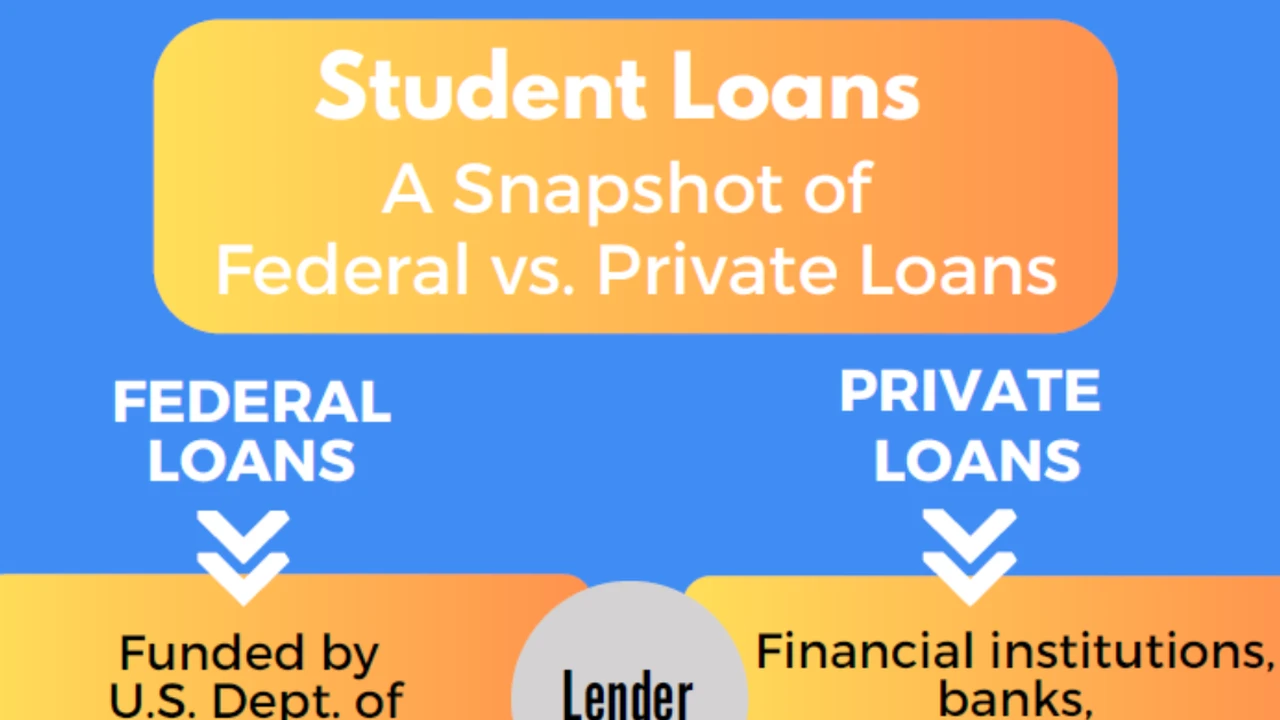

Federal student loans are issued by the U.S. Department of Education. They come with a range of benefits and protections that private loans typically don't offer. These loans are often the first choice for students because of their favorable terms and borrower-friendly features. There are several types of federal student loans, each with its own specific characteristics.

Direct Subsidized Loans For Undergraduate Students with Financial Need

Direct Subsidized Loans are available to eligible undergraduate students who demonstrate financial need. The key benefit here is that the U.S. Department of Education pays the interest on these loans while you're in school at least half-time, during your grace period (usually six months after you leave school), and during periods of deferment. This means you borrow less in the long run because interest isn't accruing while you're focused on your studies. The interest rate for these loans is fixed, meaning it won't change over the life of the loan. For the 2023-2024 academic year, the interest rate for undergraduate Direct Subsidized Loans is 5.50%. There's also an origination fee, which is a small percentage of the loan amount deducted before the funds are disbursed. For loans disbursed on or after October 1, 2023, and before October 1, 2024, this fee is 1.057%.

Direct Unsubsidized Loans For All Eligible Students Regardless of Need

Direct Unsubsidized Loans are available to both undergraduate and graduate students, and financial need is not a requirement. Unlike subsidized loans, you are responsible for paying all the interest that accrues on an unsubsidized loan from the time it's disbursed until it's paid in full. If you choose not to pay the interest while you're in school or during your grace period, it will be capitalized, meaning it will be added to your principal loan amount, and future interest will be calculated on that larger sum. This can significantly increase the total cost of your loan. The interest rates are fixed but differ based on your student status: 5.50% for undergraduates and 7.05% for graduate students for the 2023-2024 academic year. The origination fee is the same as for subsidized loans: 1.057%.

Direct PLUS Loans For Graduate Students and Parents of Undergraduates

Direct PLUS Loans are designed for graduate or professional students (Grad PLUS) and parents of dependent undergraduate students (Parent PLUS). These loans can cover up to the cost of attendance minus any other financial aid received. A credit check is required for PLUS loans, but the criteria are less stringent than for private loans. If you have an adverse credit history, you might still be able to get a PLUS loan with an endorser (someone who agrees to repay the loan if you don't) or by documenting extenuating circumstances. The interest rate for PLUS loans is higher than for subsidized or unsubsidized loans, fixed at 8.05% for the 2023-2024 academic year. The origination fee is also higher, at 4.228%.

Key Benefits of Federal Student Loans Understanding the Advantages

Federal student loans offer several significant advantages that make them a preferred choice for many students:

- Fixed Interest Rates: All federal student loans have fixed interest rates, meaning your interest rate won't change over the life of the loan. This provides predictability in your monthly payments.

- Income-Driven Repayment (IDR) Plans: Federal loans offer various IDR plans that can adjust your monthly payments based on your income and family size. This can be a lifesaver if you graduate and find yourself in a low-paying job.

- Loan Forgiveness Programs: Certain federal loan programs, like Public Service Loan Forgiveness (PSLF), can forgive the remaining balance of your loans after a certain number of qualifying payments if you work for a qualifying employer.

- Deferment and Forbearance Options: If you face financial hardship, you can temporarily postpone or reduce your loan payments through deferment or forbearance. Interest may still accrue during these periods, but it provides a safety net.

- No Credit Check (for most): Direct Subsidized and Unsubsidized Loans do not require a credit check, making them accessible to students with limited or no credit history.

- Death and Disability Discharge: Federal student loans are discharged (canceled) if the borrower dies or becomes totally and permanently disabled.

Understanding Private Student Loans Your Alternative Funding Source

Private student loans are offered by banks, credit unions, and other private lenders. They are not backed by the federal government and typically have fewer borrower protections and less flexible repayment options compared to federal loans. Private loans are often used to bridge the gap between the cost of attendance and the amount covered by federal aid, scholarships, and grants.

Interest Rates Fixed vs Variable and Their Implications

Private student loans can come with either fixed or variable interest rates. A fixed interest rate remains the same throughout the life of the loan, offering predictable monthly payments. A variable interest rate, on the other hand, can fluctuate based on market conditions (often tied to an index like the prime rate or LIBOR). While a variable rate might start lower than a fixed rate, it can increase over time, leading to higher monthly payments and a greater total cost for the loan. This introduces an element of risk that you need to be comfortable with.

Credit Requirements and Cosigners Understanding the Need

Unlike most federal loans, private student loans almost always require a credit check. Lenders will assess your creditworthiness to determine your eligibility and interest rate. Since many students have limited or no credit history, a cosigner is often required. A cosigner is typically a parent or another creditworthy adult who agrees to be equally responsible for the loan if the primary borrower fails to make payments. Having a cosigner with good credit can help you qualify for the loan and potentially secure a lower interest rate.

Repayment Options and Flexibility What to Expect

Private student loan repayment options are generally less flexible than federal loans. While some lenders may offer deferment or forbearance in specific circumstances, these options are usually limited and at the discretion of the lender. Income-driven repayment plans are typically not available for private loans. Repayment usually begins shortly after graduation, or sometimes even while you're still in school.

Comparing Federal vs Private Student Loans A Side-by-Side Look

Let's put federal and private student loans head-to-head to highlight their key differences:

| Feature | Federal Student Loans | Private Student Loans |

|---|---|---|

| Lender | U.S. Department of Education | Banks, credit unions, private lenders |

| Interest Rates | Fixed | Fixed or Variable |

| Credit Check | Not required for most (except PLUS loans) | Required for all, often needs a cosigner |

| Financial Need | Required for Subsidized Loans | Not a factor |

| Repayment Plans | Income-driven, standard, extended, graduated | Generally less flexible, standard repayment |

| Loan Forgiveness | Available (e.g., PSLF) | Rarely available |

| Deferment/Forbearance | Broad options | Limited options, lender discretion |

| Interest Accrual in School | Subsidized: No; Unsubsidized/PLUS: Yes | Yes, for most |

| Origination Fees | Yes, typically lower | Varies by lender, can be higher or none |

| Bankruptcy Discharge | Very difficult to discharge | Very difficult to discharge |

When to Consider Federal Student Loans Your First Stop for Funding

For most students, federal student loans should be your first option when seeking financial aid. Here's why and when to prioritize them:

- You have demonstrated financial need: If you qualify for Direct Subsidized Loans, take advantage of the government paying your interest while you're in school. It's free money in the long run!

- You want flexible repayment options: The income-driven repayment plans offered by federal loans provide a crucial safety net if your post-graduation income is lower than expected.

- You're unsure about your career path: If you might pursue a career in public service, the PSLF program could be a significant benefit.

- You have limited or no credit history: Federal Direct Subsidized and Unsubsidized Loans don't require a credit check, making them accessible to all eligible students.

- You want predictable payments: Fixed interest rates mean you'll know exactly what your payments will be from the start.

When to Consider Private Student Loans Filling the Funding Gap

Private student loans typically come into play after you've exhausted all federal aid options, scholarships, and grants. They can be a necessary tool to cover the remaining costs of your education. Here are scenarios where private loans might be considered:

- You've reached federal loan limits: Federal loans have annual and aggregate limits. If your cost of attendance exceeds these limits, private loans can help cover the difference.

- You don't qualify for federal aid: Some students, particularly international students who don't meet specific eligibility criteria, may not qualify for federal student aid. Private loans become a primary option in these cases.

- You have excellent credit (or a cosigner with excellent credit): If you or your cosigner have a strong credit history, you might qualify for competitive interest rates on private loans, potentially even lower than some federal PLUS loan rates.

- You're pursuing a specific program not covered by federal aid: While rare, some specialized programs might have unique funding needs that private loans can address.

Choosing a Private Lender What to Look For

If you decide to pursue private student loans, it's essential to shop around and compare offers from multiple lenders. Don't just go with the first one you find. Here are some key factors to consider:

Interest Rates and Fees Understanding the True Cost

Compare both fixed and variable interest rates. While a variable rate might seem appealingly low initially, remember the risk of it increasing. Look for lenders that offer competitive fixed rates. Also, be aware of any fees, such as origination fees, application fees, or late payment fees. Some lenders pride themselves on having no origination fees, which can save you money upfront.

Repayment Terms and Options Flexibility Matters

Inquire about the available repayment terms. Do they offer in-school payment options (e.g., interest-only payments while studying)? What are the deferment or forbearance policies in case of financial hardship? While private loans are less flexible than federal, some lenders offer more generous terms than others.

Borrower Benefits and Discounts Look for Added Value

Many private lenders offer borrower benefits or discounts. These can include interest rate reductions for setting up automatic payments (often 0.25% off), cosigner release options (allowing your cosigner to be removed from the loan after a certain number of on-time payments), or even small principal reductions for good academic performance. These can add up to significant savings over the life of the loan.

Customer Service and Reputation Read Reviews

Research the lender's reputation for customer service. Read online reviews and check with consumer protection agencies. You want a lender that is responsive, transparent, and easy to work with, especially if you encounter issues during repayment.

Specific Private Loan Products and Their Features A Closer Look

Let's look at some popular private student loan providers and what they offer. Keep in mind that interest rates and terms are subject to change and depend on your creditworthiness and the market.

Sallie Mae Student Loans A Popular Choice

Sallie Mae is one of the largest and most well-known private student loan lenders. They offer a variety of loan products for undergraduate, graduate, and even career training students. They are known for their competitive rates for borrowers with excellent credit and their flexible repayment options, including deferred payments, interest-only payments, or fixed payments while in school. They also offer a cosigner release option after 12 consecutive on-time principal and interest payments. Sallie Mae often has no origination fees. Their interest rates can vary widely based on credit score, ranging from around 4% to 16% APR for fixed rates and 5% to 17% APR for variable rates (as of late 2023/early 2024, these are illustrative and subject to change).

Discover Student Loans Simplicity and Rewards

Discover offers private student loans with no application or origination fees. They are known for their 1% cash reward on each new loan for good academic performance (maintaining a 3.0 GPA or higher). They offer both fixed and variable interest rates. Discover also provides a 0.25% interest rate reduction for setting up automatic payments. Their repayment options include deferring payments until after graduation or making interest-only payments while in school. Interest rates typically range from 4% to 15% APR for fixed and 5% to 16% APR for variable, depending on credit.

College Ave Student Loans Customizable Options

College Ave is popular for its highly customizable loan options. You can choose your loan term (from 5 to 15 years) and your in-school payment option (full deferment, interest-only, or flat $25 payments). They offer loans for undergraduate, graduate, and even parent loans. College Ave also has no application or origination fees. They offer competitive fixed and variable rates, often starting lower than some competitors for well-qualified borrowers. Their rates can range from 3.5% to 14% APR for fixed and 4.5% to 15% APR for variable, again, highly dependent on credit.

CommonBond Student Loans Focus on Community

CommonBond offers private student loans with a focus on social impact, often contributing to educational initiatives. They provide loans for undergraduate and graduate students, including MBA, law, and medical school loans. CommonBond offers both fixed and variable rates, and they have a unique hybrid rate option that starts as a fixed rate and then converts to a variable rate. They also offer a 0.25% autopay discount and a cosigner release option. Their rates are generally competitive, often in the 4% to 13% APR range for fixed and 5% to 14% APR for variable.

SoFi Student Loans Refinancing and New Loans

SoFi is well-known for student loan refinancing, but they also offer new private student loans for undergraduate and graduate students. They boast no fees (no origination fees, no late fees, no insufficient funds fees). SoFi offers competitive fixed and variable interest rates and a 0.25% autopay discount. They also have a strong focus on career support and networking for their members. Their rates can be very competitive for borrowers with excellent credit, often starting from 3.5% to 12% APR for fixed and 4.5% to 13% APR for variable.

The Application Process What to Expect

Whether you're applying for federal or private loans, understanding the application process is key.

Federal Loan Application The FAFSA First

To apply for federal student aid, you must complete the Free Application for Federal Student Aid (FAFSA). This form collects information about your financial situation and determines your eligibility for federal grants, scholarships, work-study, and federal student loans. It's crucial to complete the FAFSA as early as possible each year, as some aid is awarded on a first-come, first-served basis. Your school will then send you a financial aid offer letter detailing the aid you're eligible for.

Private Loan Application Direct to Lender

For private student loans, you apply directly to the bank, credit union, or online lender. This typically involves an online application where you'll provide personal information, financial details, and often, information about your cosigner if you have one. The lender will then perform a credit check. If approved, you'll receive a loan offer with the proposed interest rate and terms. It's important to compare these offers carefully before accepting.

Repayment Strategies Planning for Your Future

Once you've secured your loans, understanding repayment is paramount. Don't wait until graduation to think about it!

Understanding Your Loan Servicer Who to Pay

For federal loans, once your loan is disbursed, it will be assigned to a loan servicer (e.g., Nelnet, MOHELA, Aidvantage). This is the company you'll make payments to and who will manage your loan. For private loans, the lender you borrowed from will typically be your servicer, though some may use third-party servicers.

Choosing a Repayment Plan Federal Flexibility

Federal loans offer various repayment plans. The Standard Repayment Plan has fixed payments over 10 years. Income-Driven Repayment (IDR) plans adjust your payments based on your income and family size, which can be very helpful if your post-graduation income is low. There are also Graduated Repayment (payments start low and increase over time) and Extended Repayment (longer terms for larger loan balances). Choose the plan that best fits your financial situation.

Private Loan Repayment Less Flexibility

Private loan repayment is generally less flexible. Most private loans have a standard repayment schedule, often 10 to 15 years, with fixed monthly payments. Some lenders may offer limited deferment or forbearance options, but these are usually for specific circumstances and at the lender's discretion. Always understand these terms before signing.

The Importance of Financial Literacy and Planning

Regardless of whether you choose federal or private loans, financial literacy is your best friend. Understand the terms of your loans, know your interest rates, and be aware of your repayment obligations. Create a budget, track your spending, and try to minimize the amount you borrow. Every dollar you don't borrow is a dollar you don't have to pay back with interest. Consider making interest-only payments while in school if your budget allows, especially for unsubsidized and private loans, to reduce the total cost of your loan. This proactive approach will set you up for greater financial success after graduation.

Ultimately, the best student loan option depends on your individual circumstances, financial need, credit history, and future career plans. Always prioritize federal loans first due to their borrower protections and flexible repayment options. If you still have a funding gap, then carefully research and compare private loan options to find the one that best suits your needs. Borrow wisely, plan ahead, and you'll be well on your way to achieving your academic and financial goals.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)